Influence to Infrastructure: How Creators Are Reshaping the Economy

The dominant cultural image of the content creator is that of an individual producing high-quality video from a domestic environment, achieving global visibility with limited resources. This representation is accurate for many practitioners, particularly during the early stages of their careers. For the largest creators, however, the image is not merely incomplete: it is structurally misleading, and obscures the trajectory along which the creator economy is currently moving.

What a brand actually buys when it commissions a creator video

The most efficient starting point is monetary value, which flattens all qualitative judgments onto a single dimension. Suppose a video produced by a content creator costs 100 units. The unit is arbitrary; what matters is the comparative structure of the transaction.

A typical mid-sized enterprise is accustomed to paying 100 units for a corporate video produced by a local production company. The expenditure purchases the video and nothing else. When the same 100 units are allocated to a content creator, the brand acquires three distinct components in a single bundle.

The first component is the testimonial function: the brand acquires the association with the creator as a public figure, along with the values that the creator’s audience attributes to them. The second is the production of the video itself. The third is the amplification provided by the creator’s audience.

Component one: the testimonial and brand association

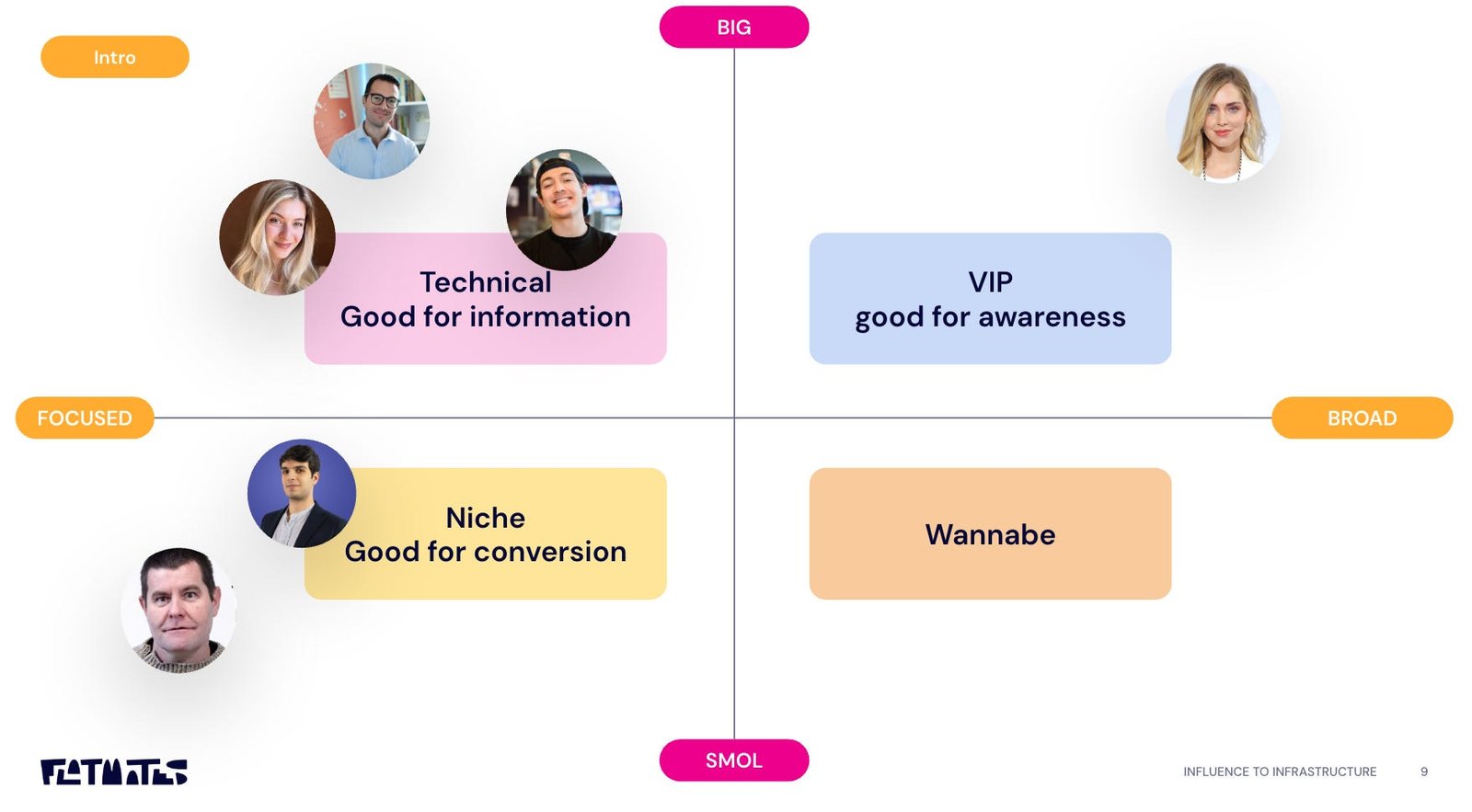

When a company associates itself with a creator, it absorbs the values that the creator embodies in the eyes of their audience. Different creators are appropriate for different brands. The selection problem is one of affinity: a brand operating in family-oriented categories will look for creators whose values align with family and childhood audiences, and will avoid creators whose public persona is centred on adult or transgressive content. The theoretical mapping is straightforward; the empirical execution is more complex.

Creators also occupy different positions in the funnel. When the campaign objective is brand awareness, the selection logic favours creators with large and demographically broad audiences. Generalist creators, however, lack credibility on specialised topics: a financial product is better promoted by a creator with a track record in entrepreneurship and business analysis than by a lifestyle creator with comparable reach. When the objective is conversion, that is, direct sales attribution, creators with smaller but highly engaged communities frequently outperform larger but more diffuse audiences.

Component two: content production

The second component is the production of the content. In this dimension, creators are in direct competition with traditional production companies and creative agencies, which can charge substantially higher day rates for production alone.

Agencies are typically effective at producing content for television or corporate events. They tend to underperform on YouTube because they do not fluently reproduce the platform’s grammar: the editing rhythm, the speed ramping, the inflections of address, and the conventions of self-reference that characterise the medium. Creators, by contrast, have grown up within that grammar and optimise content for the platforms on which it is meant to perform.

When a brand commissions a video from a creator, it accepts a degree of editorial concession. The creator is not an external director executing a brief: they do not work from a script, nor present a storyboard for approval. In exchange for reduced control, the brand obtains content that is optimised for the channel and its community, which is not a trivial outcome.

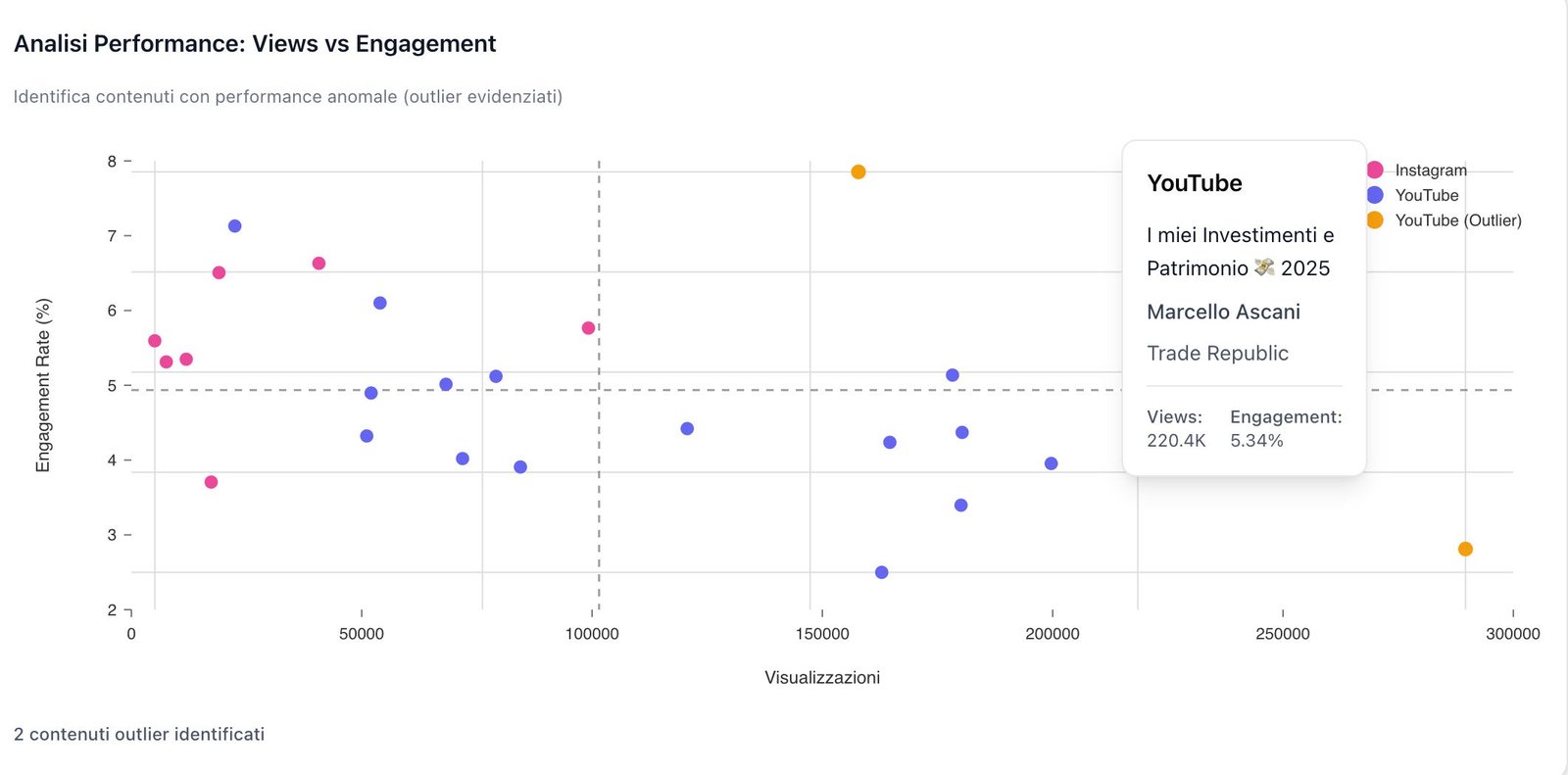

Flatmates structures content production around three commercial formats with distinct cost profiles. The first is the dedicated video, in which the creator covers a brand’s product or service as the central topic of the video, as in Marcello Ascani’s full review of Trade Republic. The second is the mention, in which the brand appears for a limited segment within a video focused on a different topic. The Tintoria podcast’s embedded segment on NordVPN, within an interview with Jake La Furia, illustrates the format. The third is the individual post, which functions as a tactical activation complementary to longer formats and often extends visibility to adjacent social platforms.

The relationship between cost and content density is monotonic: the more the content is constructed around the brand, the more expensive it becomes. There is, however, a counterintuitive finding. At equivalent cost, when the brand grants the creator full editorial autonomy, the resulting video is often substantially more effective in terms of views and engagement. Conversely, when the brand requires the creator to read a pre-written script, the video tends to underperform reliably.

A significant portion of the work conducted by an agency such as Flatmates consists in identifying the variables that distinguish high-performing content on specific channels, so that those variables can be reproduced. The exercise is difficult. A useful heuristic is to look for outlier videos, those whose view counts or engagement substantially exceed channel averages, and reverse-engineer the elements that account for the divergence.

Component three: community and amplification

The third component is the community, defined as the population of followers, subscribers, or regular viewers attached to the creator’s channel. The community determines the expected amplification, that is, the number of people likely to be exposed to a piece of content once it is published.

In traditional media procurement, amplification is purchased separately. A brand invests in media budget across specific channels in order to determine how many people will see a given message. The expenditure on television or print media operates on this principle.

In the creator economy, amplification is bundled into the price. A brand may work with a creator who has one thousand followers or one million, and will typically pay more for the larger audience.

The simplicity is deceptive. Several factors complicate the relationship between follower count and effective reach.

First, follower count is no longer a reliable metric on any platform. The intermediation of algorithmic ranking systems between subscribers and impressions means that effective reach is decoupled from nominal audience size.

Second, follower count is no agnostic indicator of fit. The audience of a creator may be inappropriate for a given brand for geographic or demographic reasons. Spanish-language creators, for example, often have substantial Latin American audiences, which are not relevant to brands distributed only in Spain.

Third, engagement rates vary substantially across channels, and dormant audiences do not convert into observable outcomes regardless of their size.

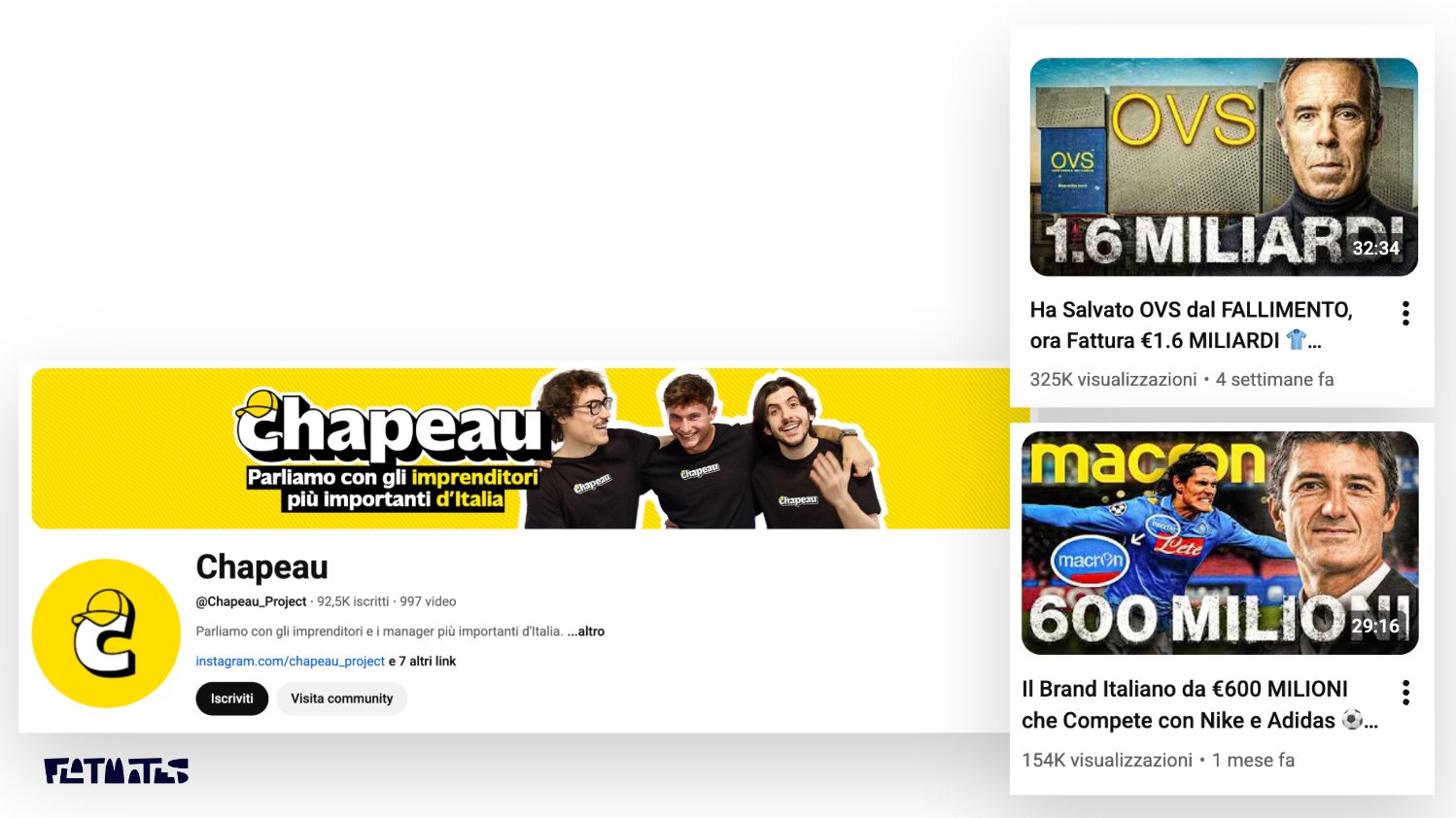

Fourth, when the creators are particularly skilled and the channel is relatively young, view counts may exceed follower counts by a significant multiple. The Chapeau channel provides a useful illustration: with approximately 100,000 subscribers, individual videos regularly reach 300,000 views. The phenomenon is more frequent on YouTube than on Instagram because YouTube functions as an interest platform, in which content is surfaced based on topical affinity, whereas Instagram operates closer to a social graph model in which distribution is constrained by existing connections.

A more sophisticated analytical approach examines average views per recent video rather than subscriber count. Flatmates typically calculates the median view count of the last ten videos and uses that figure to project CPM and expected reach.

The cost structure behind a creator video

The production of content at the level of an established creator is not trivial. Maintaining a public figure requires sustained investment of time and resources: physical conditioning, dental care, dietary discipline, and continuous attention to the quality of the published output. The construction of the public persona itself often involves producing content without immediate compensation, as part of long-term reputation building.

The trajectory carries non-trivial reputational risks. The relationship between a creator and their audience is built on trust, and missteps are typically interpreted as betrayals rather than as ordinary errors. A creator who has built a brand around impeccable entrepreneurial conduct will face disproportionate consequences from a single episode of poor personnel management. A creator whose public position centres on opposition to verbal violence will face significant reputational cost for a single intemperate public statement.

Beyond persona maintenance, the production of a single video carries hard costs comparable to those of a traditional production company: travel, food, equipment, and so on. Other costs are less visible. Many of the creators with whom Flatmates collaborates work in long-form explanatory and journalistic formats, in which the writing process alone may require several weeks of work per video.

Production complexity scales with the format. Interviews and reportage require larger teams as their scope expands, and the same logic applies to entertainment-oriented content.

The relevant point is structural. The dominant image of the creator as a single individual working alone is accurate for most practitioners. According to data published by AICDC and Assoinfluencer in their I-Com report, Italy hosts approximately 37,700 content creators, and for most of them the solo-practitioner model is empirically accurate.

For the top percentile, however, the structure is substantially different. Marcello Ascani, used here as a reference because he shares office space with Flatmates, publishes approximately 100 videos per year. His team has at least two videos in production at any given week, manages frequent travel, and handles a high frequency of brand agreements.

This workload requires a structured team covering logistics, social media management, and other adjacent functions. Video production itself remains the most intensive activity and requires multiple specialists, beginning with sound design: on YouTube, audio quality is frequently more determinative of viewer retention than visual quality.

A notable trend is that a significant share of established content creators are organising their operations to resemble small production companies. The team supporting GioPizzi numbers six or seven people; the team supporting Marcello Ascani exceeds thirteen.

From content creator to structured company

The transition from individual YouTuber to a corporate structure employing a substantial team is symptomatic of a broader shift within the creator economy. YouTube has existed for twenty years, originated as a vehicle for individual expression, and has evolved into a substitute for significant portions of the global information industry.

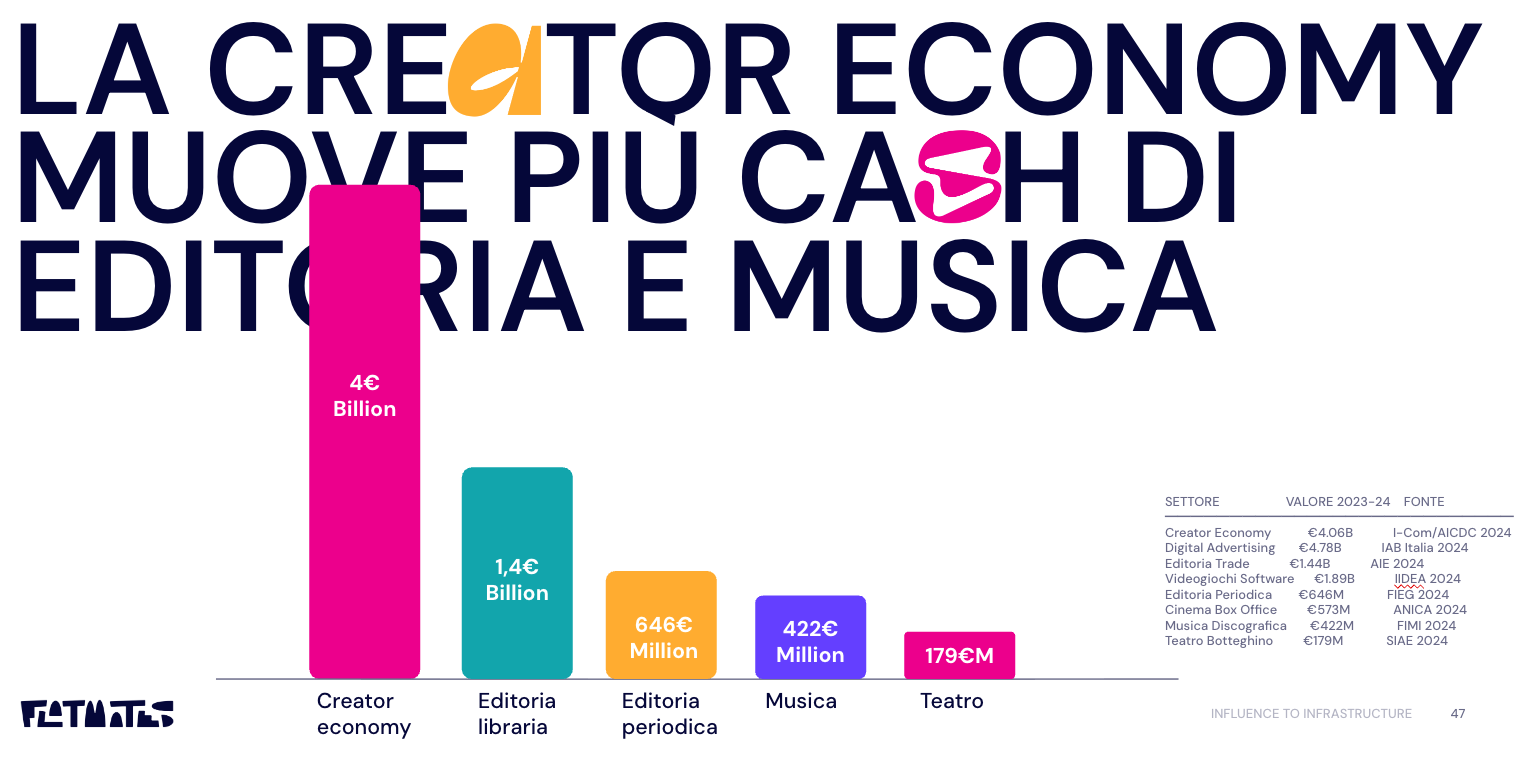

In Italy, the most recent figures place the value of the creator economy at approximately 4.06 billion euros for 2024, according to the AICDC and Assoinfluencer report. Instagram accounts for the largest share at 3.3 billion, followed by TikTok at 446.88 million and YouTube at 279.65 million. The sector supports 18,110 direct jobs, a figure that rises to 51,382 when indirect employment is included.

The economic structure of creator monetisation is frequently misunderstood. Platform revenue sharing, of which YouTube’s AdSense is the most visible example, is commonly assumed to represent the primary income source. This assumption rarely holds, particularly in the Italian context. AdSense revenues depend heavily on category vertical (financial content monetises higher than culinary content), geographic distribution of audience, and video duration. For the largest creators in Italy, revenue sharing typically does not exceed 5% of total income.

The dominant revenue source is brand collaboration, which ranges from episodic formats such as individual posts or mentions to more structured arrangements including dedicated videos and ambassador relationships.

The final stage in the trajectory from individual creator to structured company is the development of proprietary products, whether digital (online courses, software, subscription services) or physical (consumer goods, retail).

Several trends within this evolution deserve attention.

First, creators increasingly seek to migrate their communities off platform, particularly when platform algorithms are unpredictable. The strategic logic is straightforward: a community accessible directly via email, SMS, or a proprietary application is less subject to algorithmic intermediation than one resident only on a third-party platform.

Second, business models based on digital services are particularly attractive because they exhibit near-zero marginal costs. The sale of one additional unit of an online course requires almost no additional expenditure, which allows for scaling that is unconstrained by production capacity.

Third, an increasing number of brands are operating as if they were creators themselves. These brands prioritise community construction over traditional advertising, work with small creators and user-generated content, and apply creator-style tactics even in highly regulated categories. MySecretCase, operating in a category where conventional advertising channels are restricted, is one example.

Fourth, creators are experimenting with increasingly differentiated business models. Datapizza, an Italian creator media company focused on artificial intelligence, generates revenue from three distinct streams: consulting services, technology and software, and recruitment.

Fifth, some established creators have built complex corporate structures composed of multiple legal entities, internalising most stages of the value chain. Clio Makeup, for instance, has internalised functions ranging from SEO to product manufacturing, and operates across four physical stores and a digital retail presence. Even when specific functions are externalised, such as advertising management, the partners involved are significant industry players: Clio Makeup works with the publishing group GEDI.

Implications

Influencer marketing emerged as a tactical instrument for directing purchase decisions, leveraging online opinion leaders of varying scale.

In the intervening years, the function of creators has expanded substantially. Their impact on the real economy, on cultural industries, and on political opinion formation now exceeds what was anticipated when the category first stabilised. The 2024 Donald Trump campaign, which incorporated extensive engagement with creator and podcast platforms including Logan Paul’s Impaulsive podcast, Theo Von, Joe Rogan, and Adin Ross, as documented by Bloomberg, demonstrated the political utility of these channels at presidential scale. The 2025 mayoral campaign of Zohran Mamdani in New York City, analysed in detail by NBC News, applied creator-style production techniques in collaboration with the agency Melted Solids, and reached primary victory through a combination of viral short-form video, community amplification, and direct engagement with content creators.

Creators perform functions historically associated with journalism, without the corresponding institutional protections or constraints. They function as entrepreneurs operating on their own account, and they construct businesses of non-trivial scale.

The relevant conclusion is that the creator economy has become a structural component of contemporary cultural, economic, and political discourse. The situation is genuinely unprecedented, and its full implications remain to be characterised. The next several years will produce significant analytical and practical opportunities for those working within and around the sector. One question already pressing on the industry — whether AI-generated and faceless creators can substitute for human ones, and in what proportion — is taken up in Manufacturing Fame.

Sources

- AICDC and Assoinfluencer, “La Creator Economy in Italia: Dinamiche, Impatti e Sostenibilità nell’Ecosistema Digitale” (I-Com report, 2024) — Source for 4.06 billion euro market size, 37,700 creators, 18,110 direct jobs / 51,382 total, platform breakdown (Instagram 3.3B / TikTok 446.88M / YouTube 279.65M).

- Marcello Ascani, full review of Trade Republic — Reference example for dedicated-video format.

- Tintoria podcast, interview with Jake La Furia featuring NordVPN segment — Reference example for mention format.

- Chapeau YouTube channel — Reference example for view-to-subscriber ratio dynamics.

- Datapizza — Reference example for diversified creator-media business model.

- The American Conservative, “Trump Reaches New Audience with Logan Paul Interview” (June 2024) — Source for Trump–Impaulsive episode (2M+ views in 24 hours on YouTube).

- Bloomberg, “How Popular YouTubers Pushed Young Male Voters Toward Trump” (January 2025) — Comprehensive analysis of the Trump 2024 podcast strategy.

- NBC News, “Zohran Mamdani’s social media strategy was about more than viral videos” — Source for the Mamdani digital strategy and collaboration with Melted Solids.